I’m sure you’ve heard you should save and invest your money for the future. But what exactly is “investing” and why should you care?

There are two primary reasons for investing money:

You want to generate current or future income; or

You want to grow a pot of money into an even bigger pot of money over time.

The second reason was my goal when I started investing at age 24. As I explain in this blog post, by living below my means and investing what I saved in the stock market, I was able to grow my wealth from $1,600 to $1 million over 15 years.

But how are you supposed to invest money if you are living paycheck to paycheck or have no money left over each month after paying your bills? The answer is that you either have to decrease your expenses or increase your income so you can put money in an investment or retirement account each year. If you never invest the money you earn or are given, you will almost certainly run out of money when you are older.

Think of it this way: it costs you money to live each month. You may pay rent or have a mortgage payment. You may have phone, gas, electric, cable, and Internet bills. You have to fill up your car at the gas station or pay for public transportation. You have to eat, right?

You have to earn or receive enough income in order to pay for your living expenses. You may work at a full- or part-time job. You may receive child support or alimony.

While you will always need money to pay your monthly living expenses, you might not always earn or receive enough money to pay them. How often do you encounter an 80-year-old woman who still goes to work every day? Have you ever wondered how a woman who is too old to work pays her bills? Does money just mysteriously appear in her bank account each month?

A few years ago a woman in her late 40’s approached me after a talk I gave on investing. She informed me she was recently divorced and had received a settlement of $600,000. (Her husband didn’t want to pay her monthly spousal support so he made an upfront lump-sum payout to her instead.) She didn’t want to work and didn’t think she needed to ever work again because $600,000 was a lot of money and would last her for the rest of her life, especially if she lived very frugally. In this three-minute video I explain how I concluded that if she didn’t invest her money, her $600,000 would be depleted by the time she turned 65. Had she worked with me or another financial advisor to invest that $600,000, not only would she have been able to generate monthly income from interest, dividends and option premium to pay her bills, but the remaining funds could also be invested to last longer.

It is imperative to save and invest your money. If you put a modest amount of money in a retirement account each year for 20, 30 or 40 years — while making wise investment decisions — you can build a pot of money that is large enough so you can withdraw funds every month to pay your living expenses once you reach retirement age. Social security (if you qualify to receive it) will not come close to covering your living expenses when you are in your 60’s and beyond. The average social security recipient receives roughly $16,000 a year. Could you live on that? No, I didn’t think so. However, if you were to receive thousands of dollars from your retirement account each year, that could make the difference between living in poverty and living comfortably.

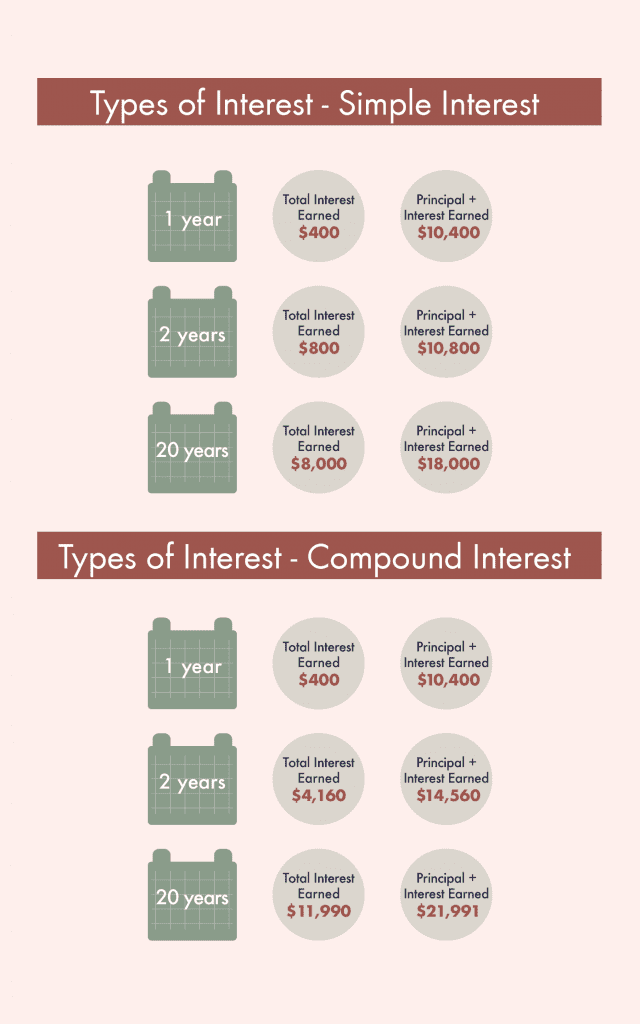

Once you learn how compound interest works, you are going to kick yourself if you aren’t already in the habit of regularly investing some of the money you earn. First, you need to understand how “simple interest” works. Imagine you put $10,000 in a savings account that earned 4% per year. After one year, you would receive $400 in interest and your account would be worth $10,400.

If you earned simple interest for 20 years, you would receive $400 x 20 (or $8,000) in interest. That means that in 20 years your $10,000 would be worth $18,000. But if you earned compound interest, in 20 years your $10,000 investment would be worth $21,991. With compound interest even your interest earns interest!

Here’s where compound interest gets exciting: instead of making just one deposit of $10,000, what if you were able to add another $1,000 to the savings account each year? In 20 years your account would be worth $51,689. What a difference!

The problem you will find is that no savings account currently pays 4% interest. You might be able to find a bank that pays 1% or 1.5% interest on money in a savings account. If you are willing to lock up your money for one or two years you can probably earn north of 2% interest by investing in a certificate of deposit (CD).

You can’t grow wealth by leaving your money in one of these bank products. It’s not much better than leaving your money under a mattress. Interest rates, although rising, are still near historical lows. If you want your money to grow over time, you need to take investment risk. The hope is that your initial investment (principal) might grow, but it also might go down in value. As a new investor, you’ll learn pretty quickly that investments that have the potential to deliver higher rates of return often fluctuate in value from year-to-year or even day-by-day.

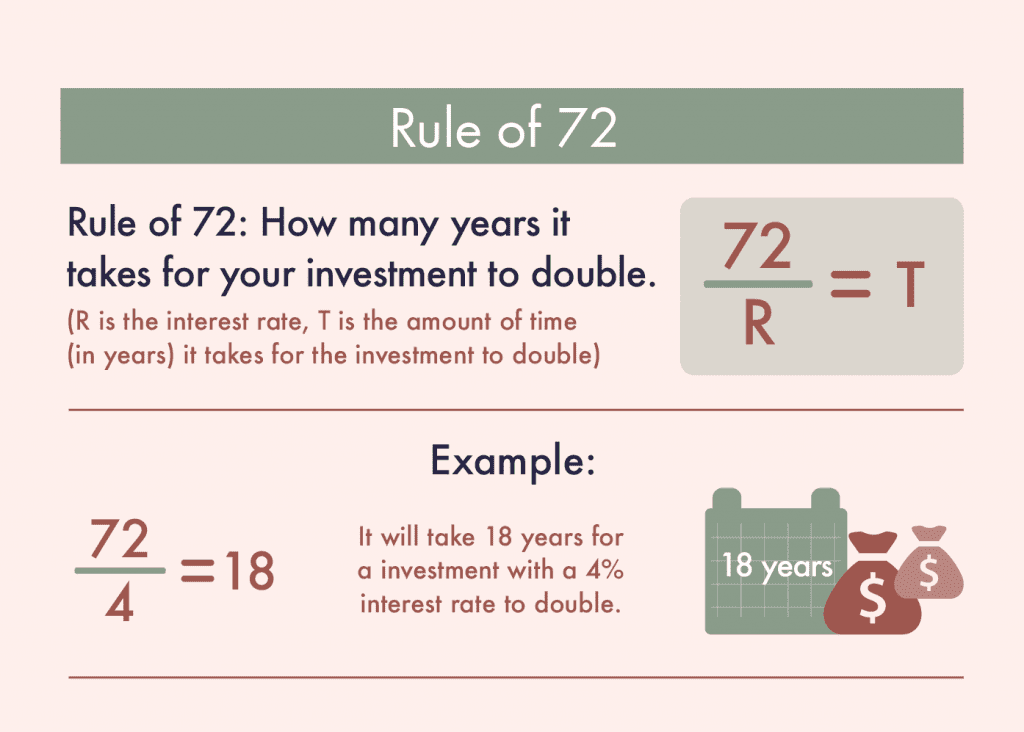

In the three-minute video above, I explain the “Rule of 72” which is a quick way to calculate approximately how many years it would take to double your money when invested at a certain annual interest rate or generating a certain annual rate of return. For example, if you were to find an investment that earns a 7.2% annual rate of return, your money would double in approximately 10 years. However, if you were to invest in a savings account that generates only a 1% annual rate of return, it would take 72 years for your money to double.

Most people think real estate is a good investment. It’s one of the rationales people use when deciding to buy a home instead of renting. Real estate can turn out to be a bad investment if you sell it at a price lower than what you paid for it. You might have to sell your home if you (or your spouse) lose a job, get divorced, or cannot make your mortgage payment. Please do not assume real estate is a safe investment. Real estate prices usually go up over time, but not necessarily at the specific time you need to sell.

Real estate also carries liquidity risk which means you can’t liquidate the asset very quickly to obtain cash. When you invest in publicly-traded securities such as stocks and bonds, you usually receive cash within days of selling.

If you want your money to grow over time, you need to take investment risk.

It’s also very expensive to sell real estate. On a $500,000 house, 6% (which is $30,000) might go to brokers’ fees and other closing costs. Compare that with selling $500,000 worth of a diversified stock portfolio. Depending on how many positions are held, the sales commission could be less than 50 bucks.

I prefer investing in stocks and exchange-traded funds (ETFs) over physical real estate. Through ETFs, I can have exposure to many asset classes including U.S. and foreign stocks; bonds; master limited partnerships; commodities such as oil, silver or gold; and even real estate through real estate investment trusts.

The options for investing are endless, but most people stick to the basics: mutual funds, stocks, bonds, and ETFs.

Mutual funds are like the training wheels of investing. If you contribute to a retirement plan offered by your employer such as a 401(k), 403(b), or thrift savings plan (TSP), your money is most likely invested in mutual funds. If you don’t plan to retire for at least ten years, you probably have most of your money invested in a stock mutual fund. If you plan to retire in only a few years, you probably have most of your money in a bond mutual fund. Or you may invest in a combination of several funds. Sometimes employers make it easy to choose by offering target date retirement funds.

When you purchase a share of company stock, you become a shareholder of that company. You might also receive quarterly dividends. Annual returns on stocks can vary widely. But if you are investing for a 20 or 30 year period, for planning purposes you might want to assume a seven to nine percent average annual return. This return might be comprised of both capital appreciation as well as reinvestment of quarterly dividends where dividend income is used to purchase additional shares of stock. There is no guarantee, however, that stocks will continue to generate rates of return as high as experienced in past 20 to 30 year windows.

When you invest in a bond, you are typically loaning money to a corporation or government or quasi-government entity. Bonds have risks too although they are generally seen as less risky than stocks. While they may pay consistent interest, they may also appreciate or depreciate in terms of price if not held to term.

ETFs are like mutual funds but with a whole host of benefits that are too detailed for this article.

There have been real estate market crashes as well as stock market crashes. Even supposed “safe” bonds can go down in value. So if you need cash to pay for critical living expenses in the next two to three years – such as a down payment on a house, tuition, or medical care – this money should not be invested. However, if you are willing to sock money away for ten years or more, then you should be able to handle the ups and downs of stocks and other investments, as long as you learn how to manage your asset allocation or hire a financial advisor to help you.

Is your goal for investing to generate monthly income to use for current living expenses or is it for long-term growth of your principal? Many investors like to do one or both depending on where they are in their lives.

I have worked with couples who together own a real estate property which they rent out for income. In the divorce, each spouse wants to keep the property because it generates income. However, sometimes the net income is paltry after subtracting monthly and annual expenses such as mortgage and property tax payments and cash outlays for repairs. Regardless of the level of net rental income, there is a good chance the property will increase in value over time. This is an example of a “growth and income” strategy.

Rental real estate never appealed to me because I don’t want to deal with tenants, toilets, or trash. I prefer generating monthly income through a covered call strategy, which is the stock market equivalent of renting out property you own. In this investment strategy, you purchase shares of stock and sell call options against the stock you own. You can generate quarterly dividend income and monthly option premium. The income generated provides some cushion against loss when stock prices go down just like rental income provides some cushion against loss when housing prices go down.

I prefer generating monthly income through a covered call strategy, which is the stock market equivalent of renting out property you own.

In a divorce settlement, if one spouse keeps the real estate and the rental income, the other can take a cash buyout and generate income by investing in covered calls and/or other income-producing securities. I teach the covered call strategy in Chapter 6 of my book, Every Woman Should Know Her Options. Covered calls can also be used in an Individual Retirement Account (IRA) if the account holder desires a less risky strategy than investing in 100% stocks.

Retirement accounts are great places to invest for growth because you don’t take out income until you retire and money compounds either tax-deferred or tax-free (in the case of a Roth IRA).

If your employer offers a retirement plan, such as a 401(k), 403(b), or Thrift Savings Plan (TSP), that’s a good place to start investing, especially if your employer matches part of your contributions. Don’t pass up free money! Once you start participating, your contributions are made automatically from your paycheck. Some employers also offer a Roth 401(k). Your current federal and state income tax brackets will be factors in deciding between the traditional and Roth 401(k). Most employer-provided retirement plans offer a selection of mutual funds in which to invest.

If you are self-employed, there are a variety of retirement accounts you can establish, with my favorite being the SEP IRA due to its ease of setup. This is a convenient way to lower your taxable income which translates into paying less tax. With IRAs, you are not limited to mutual funds and have a universe of securities from which to choose.

I often recommend a Roth IRA for women in low tax brackets or those who think they may need to access some of their funds before retirement age. I also recommend the Spousal IRA for stay-at-home moms who are married.

The maximum annual contribution for a Traditional, Roth or Spousal IRA is $5,500 ($6,500 if you are over 50). If you already have money in the bank for emergencies, make 2020 the year you fully fund an IRA (assuming you qualify). If you were to invest $5,500 a year in an IRA for 20 years, depending on how conservatively or aggressively you invested it, you could end up with between $150,000 and $250,000. Make it an annual habit to contribute to a workplace retirement plan, an IRA, or both.

If you want an investment account that is not tied to retirement, you can open a brokerage account. Just be aware that you may have to pay taxes on your investment earnings each year.

There are many financial institutions that offer brokerage accounts and IRAs with no setup fees. Find this overwhelming and need some one-on-one coaching to get started? Try my Financial Empowerment package.

Disclaimer: The information contained herein is strictly for educational, informational, and illustrative purposes, and should not be considered personalized investment advice.

If you are separated or recently divorced and wish to learn more about investing and steps you can take to ensure you don’t run out of money, I invite you to take my online course. Make sure to enter WORTHY as the coupon code to get $50 off.

©2011-2024 Worthy, Inc. All rights reserved.

Worthy, Inc. operates from 25 West 45th St., 2nd Floor, New York, NY 10036